The Most Undervalued Asset in Your Life — Mom

Maren O'Neill2026-05-04T06:30:21-06:00The Most Undervalued Asset in Your Life — Mom Acknowledgment: My mom lived to 86, but dementia took her from us long before that. I never really got the chance to thank her for everything she gave me. That’s a tab I’ll never close—but I try, in my own way, to honor her with how I live. As Mother’s Day approaches, it’s easy to default to the usual gestures—flowers, a phone call, maybe a visit if you’re lucky enough to be close. Those things matter. But it’s also worth taking a quieter moment to reflect on something we don’t often put into words, especially in a financial planning world: How do you even begin to value Mom? We spend a lot of time thinking about net worth, income, and long-term planning. Yet one of the most central forces in most families doesn’t show up cleanly on any spreadsheet. And because of that, it’s often underestimated—not out of neglect, [...]

What I Think About When I Think About College Part 2

Maren O'Neill2026-04-26T19:51:34-06:00Getting Real About College (Part 2) - The College Hangover

What I Think About When I Think About College Part 1

Maren O'Neill2026-04-19T20:21:34-06:00Getting Real About College (Part 1)

Why IRA Rollovers Matter

Maren O'Neill2026-04-11T06:37:13-06:00Why IRA Rollovers Matter — and How to Avoid a Costly Mistake

$240K is the new $100K: The New Financial Reality

Maren O'Neill2026-03-29T16:26:13-06:00$240K is the new $100K: The New Financial Reality Orange is the New Black. 50 is the new 30. $240K is the new $100K. When I was a young’un, the long-held belief that accumulating $100,000 in savings or investments marks a significant step toward financial security is a relic of a bygone era, much like your VCR and landline. While a six-figure sum still represents a substantial achievement, its real purchasing power has been systematically eroded by inflation, making $240K the new $100K. At its most fundamental level, inflation is not merely a rise in prices but a decrease in purchasing power. This constant decline in value is often referred to as a "silent tax" because it diminishes the value of money without any overt action, steadily reducing the buying power of savings held in cash or low-yield accounts. Inflation is typically measured using the Consumer Price Index (CPI), a measure of the average prices paid by [...]

5 Signs Military Families May Need A Tax Professional

Maren O'Neill2026-03-21T17:57:11-06:005 Signs Military Families May Need a Tax Professional (And It’s Not Because You’re “Bad at Taxes”)

Tax Prep Is A Mirror You Didn’t Ask For

Maren O'Neill2026-03-08T17:56:05-06:00Tax Prep Is A Mirror You Didn't Ask For Here are the top 5 lessons people tend to learn a little too late, usually right as they’re signing the return. 1. Your tax refund is not a scorecard Too late realization: “Wait… why am I getting money back if I paid so much?” People finally see that: • A big refund = overpaid all year • A small refund (or bill) ≠ doing something wrong • Taxes are math, not morality The sting comes when they realize they essentially gave the IRS an interest-free loan. 2. Your paycheck lies—your tax return tells the truth Too late realization: “We make how much?” During tax prep, people finally see: • Total household income • How bonuses, side income, or promotions are stacked • Why they accidentally jumped tax brackets This is often when folks realize their withholding never adjusted as income grew. 3. Last year’s choices echo loudly Too [...]

Gift And Estate Taxes For The Common Man

Maren O'Neill2026-03-01T17:51:03-06:00Don't Panic! A Primer on the Gift and Estate Taxes for the Common Man

💰The “Retirement Smile” — How We Really Spend in Retirement 😊

Maren O'Neill2026-02-23T07:28:32-06:00💰The “Retirement Smile” — How We Really Spend in Retirement 😊 Most people assume retirement spending stays flat. In reality, it often looks like a smiley face 😄 You spend more in the early years — travel, hobbies, bucket-list adventures. Spending usually drops in the middle years — less travel, simpler routines. Then it rises again later — mostly due to healthcare and long-term care costs. Planning for retirement isn’t just about how much you’ll need — it’s when you’ll need it. A smart retirement plan flexes with your lifestyle, just like the spending smile. Fight's On! Winged Wealth Management and Financial Planning LLC (WWMFP) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or [...]

Investor Stages

Maren O'Neill2026-02-15T19:09:37-06:00Investor Stages Financial planning involves life stages for investors. Goals, risk tolerance, and priorities evolve over time, and the strategies that work well in one phase may be completely wrong in another. Rather than thinking only in terms of age, planners often focus on investor types, which more accurately reflect how money is actually used and experienced. The first stage is often called Builders or Early Accumulators. These individuals are typically in the early to mid-stages of their careers and are laying the groundwork for everything that comes next. Income may be rising, but so are obligations—student loans, rent or a first mortgage, childcare, and lifestyle costs. The primary focus here is building stability: paying down high-interest debt, establishing an emergency fund, and beginning long-term investing, even if contributions feel modest at first. For Builders, success isn’t about maximizing returns—it’s about consistency. Automating savings, capturing employer retirement matches, and creating basic protection through insurance matter far more than [...]

“One-Time” Expenses That Happen Every Year

Maren O'Neill2026-02-09T11:37:56-06:00“One-Time” Expenses That Happen Every Year Many people derail their budget each year because they fail to plan for “one-time” expenses that aren’t actually one-time at all — they’re just irregular. Weddings, new tires, kids’ school fees, holiday travel, home maintenance, annual insurance premiums, and medical deductibles all feel like surprises in the moment, but they happen with enough frequency that they should be part of a normal spending plan. When these costs aren’t anticipated, people end up dipping into savings, swiping credit cards, or feeling like their budget is constantly blowing up for reasons “outside their control.” The truth is, these expenses are predictable — we just don’t treat them that way. The solution is to build an annual or quarterly sinking fund, where you spread these costs out over the year so they’re no longer emergencies but expected events. Planning for irregular-but-inevitable costs is one of the simplest ways to create financial stability and reduce money [...]

Good Tax Planning Hygiene: Small Habits That Make a Big Difference

Maren O'Neill2026-02-01T18:57:46-06:00Good Tax Planning Hygiene: Small Habits That Make a Big Difference Tax planning isn’t about last-minute scrambling in April. It’s about maintaining good financial “hygiene” throughout the year—small, consistent actions that reduce surprises, improve efficiency, and keep more of your money working for you. The cleanest tax outcomes usually come from steady maintenance, not dramatic moves. At the core of good tax hygiene is knowing where your income actually lands. That means understanding which tax bracket you’re in today—and which one you’re likely to be in next year. Raises, bonuses, business income, stock compensation, and retirement distributions all affect the picture. When income isn’t tracked intentionally, people often miss opportunities to defer, accelerate, or reposition income more favorably. Another key habit is placing the right assets in the right accounts. Not all dollars are taxed the same. Taxable accounts, tax-deferred accounts, and tax-free accounts each play different roles. Interest-heavy or frequently traded investments may belong in tax-advantaged accounts, [...]

National Backdoor Roth Day

Maren O'Neill2026-01-26T05:40:26-06:00Do you celebrate National Backdoor Roth Day?

TSP In-Plan Roth Conversions Are Coming!

Maren O'Neill2026-01-19T20:42:59-06:00TSP will allow Roth Conversions inside the plan in 2026—here’s what you need to know!

How Much is Too Much Money In Retirement?

Maren O'Neill2026-01-11T19:13:44-06:00How Much is Too Much Money In Retirement? What’s Too Much Money in Retirement? We spend so much time asking, “Will I have enough?” But here’s the flip side — can you have too much money in retirement? The short answer: It depends on your goals. 1. “Too much” isn’t about the number — it’s about unused purpose If you’ve saved so much that you’re afraid to spend it, or you’ll never use it to improve your quality of life, then yes — you might have too much for your personal goals. Many retirees find that their biggest regret isn’t running out of money... it’s not enjoying what they worked so hard for. Ask yourself: “What’s the money for?” If it’s meant to give you freedom, experiences, and peace of mind — then not spending it misses the point. 2. The tradeoff of “too much” Having more money than you’ll ever spend can bring other challenges: Higher taxes [...]

Insure Your Phone or Your Paycheck?

Maren O'Neill2026-01-03T14:41:07-06:00Insure Your Phone or Your Paycheck? Several psychological and practical forces drive this mismatch: 1. Salience Bias: If It’s Tangible, It Feels Riskier We see our phones every day. We drop them, scratch them, and hear constant warnings to “get the extended warranty.” The risk feels real because the object is right in front of us. In contrast, the risk of losing income due to illness or injury is invisible and abstract. Even though the consequences are far worse, the scenario feels distant — so people tune it out. 2. Misjudging Probability People are more likely to insure something if they believe the risk is high. Phone damage? Very common — one survey found 66% of smartphone owners damaged their phone within a year. A long-term or temporary disability? People assume it’s unlikely, even though statistics show 1 in 4 workers will face a disability lasting longer than 90 days during their career. This mismatch in perceived vs. [...]

Where to Stash Your Cash

Maren O'Neill2025-12-14T19:30:16-06:00Cash is either trash or king, but you still need a place to put it…

Debriefing the Government Shutdown

Maren O'Neill2025-12-06T15:40:54-06:00The government shutdown is at our six, what lessons should we learn?

100 is the New Million

Maren O'Neill2025-11-02T14:16:00-06:00One hundred is the new one million. Wouldn’t you rather have one hundred?

Estate Planning in 10 Easy Steps

Maren O'Neill2025-09-28T16:24:42-06:00Think estate planning is tedious and morbid? Think again!

Are You Forgetting to Pay Less Tax?

Maren O'Neill2025-09-22T06:38:38-06:00Is your memory bloating your tax bill?

Monday Money: Should You Convert Your TSP to Roth in 2026?

Maren O'Neill2025-09-13T16:40:46-06:00The TSP will allow in-plan Roth Conversions starting 2026, should you pay more taxes now?

The College Trap

Maren O'Neill2025-08-31T16:46:11-06:00Should you retire from the military to pay for college?

Dear Lieutenant, We Have Met

Maren O'Neill2025-08-24T18:32:34-06:00What do Lieutenants Look Like When They Grow Up?

Can Military Families Skip Taxes When Selling a Home?

Maren O'Neill2025-08-16T17:44:30-06:00Want to skip taxes on the sale of your home? Section 121 can help!

How Military Families Can Understand the New Tax Law (in Haiku)

Maren O'Neill2025-08-03T19:39:13-06:00Tax laws are boring, but can Haiku save you money?

Should Military Families Open a Trump Account?

Maren O'Neill2025-07-27T17:53:30-06:00Trump coins, steaks, universities, bibles, shoes, and now “kiddie” accounts?

Should My Daughter Have a Credit Card?

Maren O'Neill2025-07-13T20:44:21-06:00Should daughters get credit cards? Probably so, but may not for the reasons you’re thinking…

New Regret Unlocked—A Vacation Not Given

Maren O'Neill2025-07-06T15:51:05-06:00Should you buy your parents a vacation?

Taxes for Teenagers

Maren O'Neill2025-06-01T16:13:17-06:00Give a kid a tax, she’ll pay for life. Teach a kid to tax, she’ll save for life!

Peak Stuff

Maren O'Neill2025-05-03T15:21:50-06:00Stuff is everywhere. Do you have enough? Too much? Is it time to declare “Peak Stuff?”

Top 10 Tax Day Fails (Haiku Edition)

Maren O'Neill2025-04-13T17:32:33-06:00Tax day is here. Some will fail, all will pay.

Buckets of Cash: Turning Your Nest Egg Into a Paycheck

Maren O'Neill2025-04-05T14:52:11-06:00Can a bucket save you from the stock market?

Depreciation for Dummies

Maren O'Neill2025-03-30T15:04:42-06:00Appreciation grows the price of your rental home, Depreciation shrinks the cost of your taxes. Here’s what you need to know about Depreciation.

Are You Skinny Dipping?

Maren O'Neill2025-03-23T14:08:21-06:00When the tide goes out, you can tell who’s been skinny dipping… do you want to get caught?

What If Your Kids are Average?

Maren O'Neill2025-03-02T11:30:09-06:00We all know our kids are above average, but what if average was excellent?

A Series of Unusual Months

Maren O'Neill2025-02-22T16:44:21-06:00Does your budget work, except in Unusual Months? Let’s fix that!

Do You Have Real Wealth?

Maren O'Neill2025-02-08T13:41:07-06:00What is wealth and how do you know if you have it?

Risky Business

Maren O'Neill2025-02-01T06:59:28-06:00There is almost no end to the risks we endure in military service. But how do we face up to investment risk?

Are you GAH or FAB?

Maren O'Neill2025-01-12T09:46:24-06:00Are you getting ahead or falling behind? How would you know?

What’s the Best College Account–529 or UTMA?

Maren O'Neill2024-12-28T17:04:58-06:00It’s time to save for college, but where should you start? A 529? A UTMA? Something else?

Back to Basics: Account Types

Maren O'Neill2024-12-15T00:11:34-06:00Investing and personal finance has too much jargon. Let’s just focus on the basics of account types!

TSP In-Plan Roth Conversions Are Coming!

Maren O'Neill2024-11-30T09:31:35-06:00TSP will allow Roth Conversions inside the plan in 2026—here’s what you need to know!

Federal Long-Term Care Insurance Program Update

Maren O'Neill2024-11-23T13:07:42-06:00If you wanted Long-term Care insurance for Christmas, you may have to wait until 2026…

Logical Conclusions

Maren O'Neill2024-11-02T05:24:57-06:00Does the rule of law matter to your TSP? Probably so…

Do Fighter Pilots Need Healthcare FSAs?

Maren O'Neill2024-10-12T08:16:32-06:00Do you need a healthcare FSA? If you dislike taxes, maybe so…

Thank Your Parents for that Tax Bill

Maren O'Neill2024-10-06T13:53:07-06:00Your parents may be conspiring to inflate your tax bill! What can you do?

One Simple Credit Card Hack to Rule Them All

Maren O'Neill2024-09-21T11:28:03-06:00Could there really be one simple credit card hack that’s better than all of the others?

Top 10 Business Mistakes Fighter Pilots Make

Maren O'Neill2024-08-31T08:43:52-06:00If you already walk on water, how hard can running a business be? Read on to find out!

Part 6: Tax Planning –What Does Financial Planning Look Like?

Maren O'Neill2024-08-24T13:41:01-06:00Tax Planning is both a long-range and short-range exercise to help suppress your lifetime tax bill—no tips for the tax man!

Part 5: Retirement Analysis Deep Dive — What Does Financial Planning Look Like?

Maren O'Neill2024-08-16T20:45:03-06:00How do we plan for life insurance needs? What if returns are lower? We can plan for that.

Part 4: Retirement Analysis Introduction–What Does Financial Planning Look Like?

Maren O'Neill2024-08-10T18:49:52-06:00Time to look at the good stuff! Turning assumptions into actionable analysis!

Part 3: What Does Financial Planning Look Like? Net Worth and Goals

Maren O'Neill2024-08-03T16:16:24-06:00Financial planning is all about goals, but how do we distill goals for accurate planning?

(PART 2) What does Financial Planning Look Like?

Maren O'Neill2024-07-27T13:34:20-06:00Saving doesn't have to be complicated... or does it?

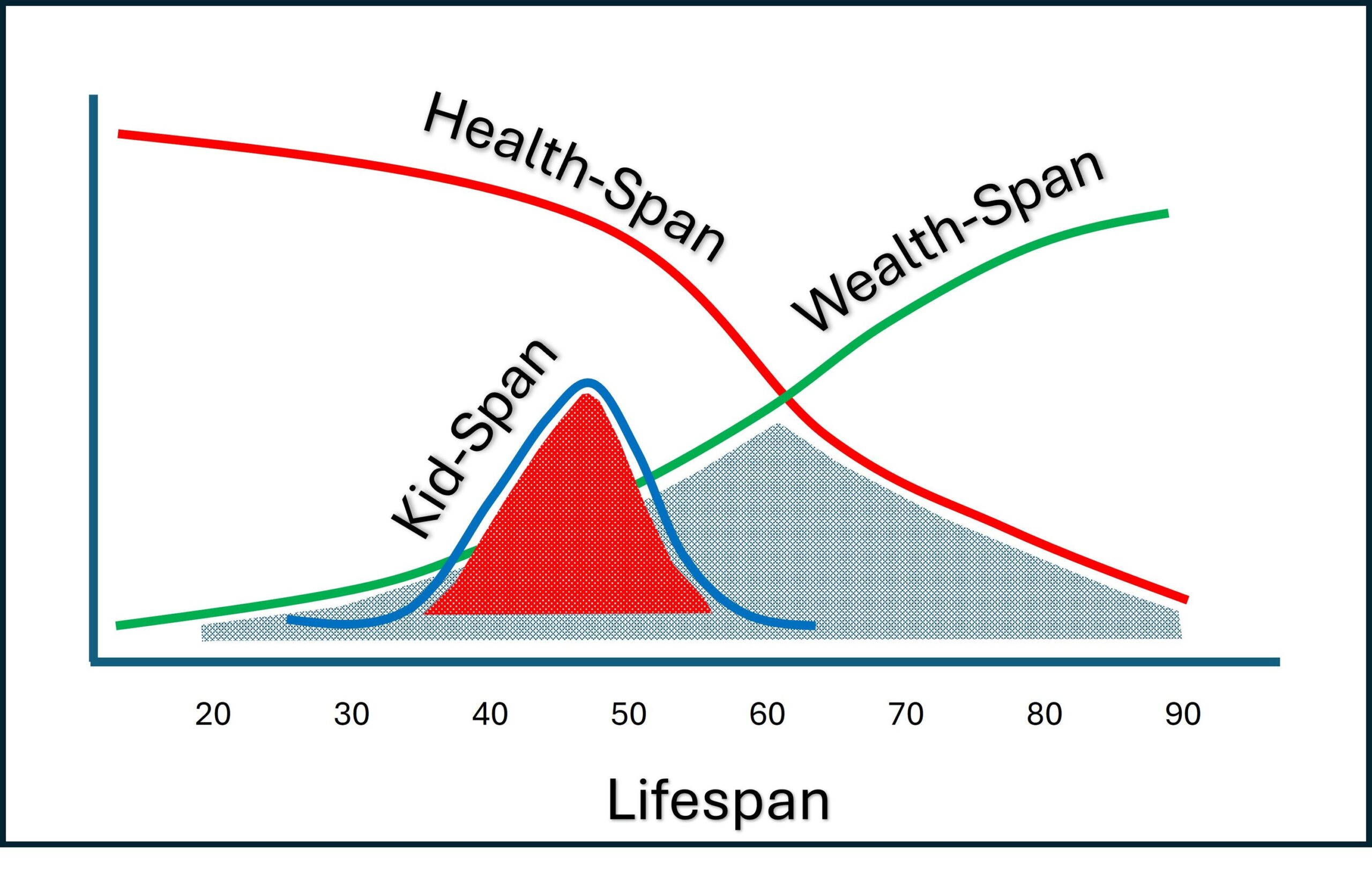

Kid-Span and the Spans

Maren O'Neill2024-06-30T13:08:01-06:00You get maybe 85 laps around the sun. How do you optimize the Wealth, Health, and Kid time during your Lifespan?

Retire to It, Not From It

Maren O'Neill2024-06-21T11:34:11-06:00Retirement has many choices. Choosing to retire may be the easiest one…

All the Single Killers…

Maren O'Neill2024-06-15T11:52:01-06:00Should you get married to pay less taxes? Probably not…

Depreciation for Dummies

Maren O'Neill2024-06-08T10:04:01-06:00Appreciation grows the price of your rental home, Depreciation shrinks the cost of your taxes. Here’s what you need to know about Depreciation.

In Memoriam

Maren O'Neill2024-05-25T14:02:00-06:00Memorial Day gives us a chance to reflect on our mission—perfecting the Union others died to preserve.

When is PAWing Okay?

Maren O'Neill2024-05-18T20:04:24-06:00Is your net worth on course, on glidepath? How much net worth should you have for your age?

Commanding Money

Maren O'Neill2024-05-12T07:26:46-06:00Commanders are busy, but they’re responsible for financial readiness too. This toolkit makes it easy to lead with money!

How Much is Mom Worth?

Maren O'Neill2024-05-05T12:57:17-06:00Mother’s day is just a few days away. Do you know how much your Mom is worth? Of course she’s priceless, but let’s peel that back a bit!

The Haiku Financial Plan

Maren O'Neill2024-04-20T04:45:29-06:00You’ve heard of one-page financial plans, note card financial plans, but what about Haiku?

Getting Real About College Again… Part 2

Maren O'Neill2024-03-23T18:51:10-06:00Hangovers are part of College, but how long should they last and do parents get them too?

Getting Real About College Again… Part 1

Maren O'Neill2024-03-14T18:31:25-06:00What is College Really For?

College SOTU (State of the Union)

Maren O'Neill2024-03-10T19:04:29-06:00College decision season is in full afterburner for seniors… what’s coming up for juniors?

The Power of Mental Accounting

Maren O'Neill2024-02-25T18:36:39-06:00If you could have a superpower, wouldn’t you want it to be mental accounting? Maybe you’re in luck…

Smooth Versus Creep

Maren O'Neill2024-02-18T08:12:10-06:00Lifestyle creep isn’t inherently bad, and consumption smoothing is definitely hard. What path should you choose?

Digital Assets—Like Stocks, but with Additional Risks

Maren O'Neill2024-02-11T18:06:19-06:00Crypto comes in ETF flavors now—is it time to buy?

Top Ten Insurance Mistakes that Fighter Pilots Make

Maren O'Neill2025-02-09T13:39:32-06:00Insurance is like Goldilocks, too much and too little are probably not the right answer…

Single Stocks—An Uncompensated Risk

Maren O'Neill2025-02-09T13:40:25-06:00Investing in single stocks can pay off big (early Apple), result in disaster (Enron), be a long-slow decline (GE), or be a roller coaster (most companies over time).

YNARB

Maren O'Neill2025-02-09T13:41:04-06:00Budgets stink. Maybe there’s another way to make your money behave… YNARB

Diversification: Always Saying You’re Sorry

Maren O'Neill2024-01-14T09:25:43-06:00It’s rare to hear that you shouldn’t diversify your investments, but really, should you?

How to Trust

Maren O'Neill2024-01-07T14:51:18-06:00You’ve decided to get a Revocable Living Trust, but what do you do now?

Short, Sweet, to the Point: 10 Quick End-of-Year Steps You Can Still Take to Max-Perform Your Money

Maren O'Neill2025-02-09T13:45:59-06:00It’s almost the end of the year, but there’s still time to max-perform your money!

Should Grandparents have 529’s?

Maren O'Neill2025-02-09T13:49:02-06:00Giving to grandkids feels good, paying for their education pays for your Social Security...so what’s the downside of a Grandparent-owned 529?

Don’t Close the Backdoor (Roth IRA)

Maren O'Neill2025-02-09T13:50:06-06:00Backdoor Roth season is in full swing. You'll need to maneuver before December 31st, so here's what you need to know about Backdoor Roth IRAs!

How Fighter Pilots Save for College

Maren O'Neill2023-09-23T15:24:06-06:00College is expensive, but there are a lot of ways to save for college. Read on to arm yourself with the best tactics!

The Premium or the Pain

Maren O'Neill2023-09-15T08:03:07-06:00We all like our cards. They provide a lot of convenience. But what do we trade for that convenience?

When is the Best Time for Roth Conversions?

Maren O'Neill2023-09-08T10:59:13-06:00Roth Conversions are mysterious until they're not. They can lower your lifetime tax bill, which is the bill you should be worrying about!

Peak Stuff

Maren O'Neill2025-02-09T13:53:30-06:00Stuff is everywhere. Do you have enough? Too much? Is it time to declare “Peak Stuff?”