Should You Prepay for College

Newsflash—college got expensive sometime last century. Military families often have a leg up in the college funding thrash compared to many civilian families. Still, one helping of Post 9/11 GI Bill only stretches so far. Prepaying college costs can be an appealing option for some families, but is it right for yours?

College Funding Options

Before diving into the pros and cons of prepaying for college, let’s look at the various common ways you can get your wingmen through their undergraduate degree.

- Post 9/11 GI Bill. If you transferred your GI bill to your dependents, you get 36 months of tuition, (most) fees, $1,000 for books per year, and a housing stipend that often leaves money left over in your bank account. The GI Bill pays the maximum in-state rate up to an inflation-adjusted cap each year, but often gets augmented by generous Yellow Ribbon funds. What’s more, academic years are often less than 9 months such that 36 months typically completes one child’s degree while leaving a little scratch for the next dependent into school.

- Service Academies. If your kiddos qualify (and like folding textiles), the academies pick up all the costs, pay a little, and offer pretty good job security on the backside.

- Scholarships. From ROTC to the $500 check earned for an essay written to the Fraternal Order of Grumpy Old Codgers Local 690, scholarships can range from a full ride to the equivalent of couch cushion money that will barely support a beer-n-pizza habit for the first semester.

- Coverdell Education Savings Account (ESA). A Coverdell is a precursor to a 529 College Savings Plan (529 from here out). A beneficiary can get one after-tax shot of $2K per year into a Coverdell. Like a Roth IRA or 529, the Coverdell funds grow tax-deferred and come out tax-free when used for qualified education expenses. Coverdell funds can be used to purchase a greater variety of investments than the offerings in most 529’s. Fairly low income limits apply to those contributing to a Coverdell and Coverdell funds must be used by age 30. Many families find that Coverdell juice is not worth Coverdell squeeze.

- Taxable investment account. If a taxable investment account throws off 2% dividends and 2% capital gains distributions, then a $100,000 account would probably pay 15% capital gains tax on $4K of income per year, or $600. Taxable accounts for college carry the benefit that they don’t have to be used for college, so $600 per year (when the account is in the six-figure range might be a reasonable cost of business for keeping funds flexible.

- Cash. If you’re a dual income family or your post-military job pays handsomely, you may just plan to pay for any college bills out of current income. This is somewhat of a no-plan game plan, but it works if you earn enough.

- Loans. Student loans come in many flavors and the least-worst versions have Uncle Sam paying the interest during college. While there are quite a few student loan forgiveness plans, trapping five or six figure debt at your kid’s six for a decade or more will probably feel like the gift that keeps on taking.

- 529 Plans. If only I could write “529 Plan” vs “Plans…” There are seemingly countless 529 plans because they are state sponsored (50 states, often 2 per state). The big picture is: contribute after-tax dollars, compound them with investments until needed, then use the original investment plus the earnings tax-free for qualified expenses. More to follow on 529 plans.

- Prepaid Plans. Technically, prepaid plans are also 529 plans as they come from the same IRS code section 529. More to follow on prepaid plans.

529 Plan Types

If you like the idea of tax-deferred growth and tax-free spending, then a 529 plan is your friend. There are three main types of 529 plans.

- Direct-sold plans are best for most families. There is no financial professional in the mix. You open an account online, drop in some cash, pick your investments and ride the stock/bond market until it’s time for college.

- Advisor-sold plans function the same as direct plans, but an advisor performs some of the labor and may earn a commission as you put new money into the account and typically earns a percentage for managing the account.

- Prepaid plans create an option to lock in today’s tuition rates at your state’s school so that you don’t worry about what inflation does to tuition when junior attends college in 18 years. Depending on what your state offers, you can pay for a prepaid plan in a lump sum or installments.

While a prepaid plan is a 529 plan, to minimize confusion going forward, we’ll use the term 529 plan for Direct and Advisor-sold plans, and prepaid plan for, well, prepaid plans.

Direct-sold and Advisor-sold Plans

Each state has its own 529 plan rules, but generally, anyone can contribute up to the annual IRS gift exclusion ($17K in 2023) for the beneficiary—parents, grandparents, neighbors, and Kardashians can all theoretically boost your kiddo’s 529. Generous givers can actually super-fund the account with 5 years worth of the IRS exclusion amount ($85K in 2023), but must wait 5 more years before contributing any more.

- Investments in these plans are mutual fund-like investments, but not the exact same funds and tickers you might buy in your IRA. Buyer beware as some state plans use expensive, actively-managed funds.

- Target-enrollment funds inside most plans give you an autopilot option such that the fund manager automatically dials back the risk (and likely return) as your child nears age 18 and enrollment. Again buyer beware as these might not meet your return needs or risk tolerance and capacity.

- These plans can have contribution limits such that upon, reaching a balance of several hundred thousand dollars, no additional funds can be contributed.

- There is no practical limit to the number of accounts that can be opened for your kiddos. You can change the beneficiary to essentially anyone in your bloodline tax free and there are no age limits for using the funds.

- The most common qualified expenses are tuition, fees, room, board (including off-campus), computers and software but there are other allowable expenses too. 529 funds can’t be used for travel which is often a sizeable college expense.

- With the new SECURE Act 2.0 passed in late 2022, unused 529 funds can be rolled to a Roth IRA for the beneficiary. The rules for this are in work and the use case will certainly have limits, including that the account must have been opened for 15 years!

- If funds aren’t needed due to scholarships (including GI Bill or Academy), you can pull out an equivalent amount of 529 funds to the scholarship amount that year and only pay income tax on the earnings (not the principal) and there is no 10% penalty. This implies tax planning to see what the extra dough will do to your AGI, MAGI(s), and taxable income.

- Finally, 529 plan funds can generally be used for up to $10K of K-12 private school tuition, but if you got a state tax deduction, your state may claw back the deduction for K-12 schooling.

Prepaid Plans

Of the limited number of states with prepaid plans, each operates its prepaid plan differently, and some still call them 529 plans or Prepaid 529 plans. The primary value proposition is that if you fully fund the plan with installment payments or a lump sum, you know you’ll have tuition covered in your state. The plans typically have options to include some level of room and board, but you’ll likely still have out-of-pocket costs. If the state has tiers of institutions such as flagship universities down to 2-year junior colleges, you can choose which level to fund, but you can’t get the flagship school at the junior college price.

- Prepaid plans do not guarantee admission to any particular school. Junior still must apply and earn admission.

- Prepaid plans generally allow you to take the money out-of-state or to a private college, but only at the level of cost for the tuition tier you purchased.

- A good reason to use a prepaid plan is to force college savings. It feels like paying a bill rather than optionally contributing towards a college path that may not even happen.

- Also, if the child doesn’t need the money (gets scholarships, doesn’t go to college, etc.), you can usually get a refund of your contributions without a tax bill (or 18 years of investment gains…).

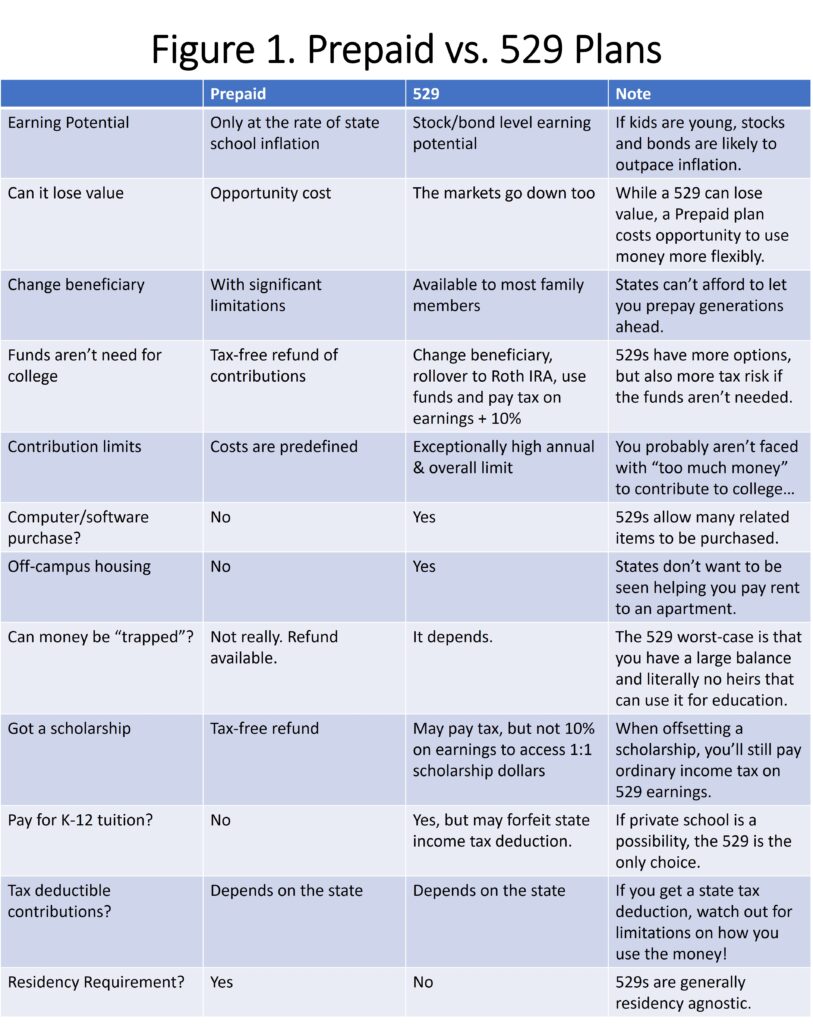

The Pros list of prepaid plans is a bit shorter than the Cons when comparing to Direct-sold and Advisor-sold plans and Figure 1 has an easy summary chart.

- Prepaid plans will not outpace inflation, but a 529 can.

- Prepaid plans focus on your state’s colleges, but your child is likely to consider private and out-of-state schools where the costs aren’t pegged to your state’s calculations.

- Prepaid plans can limit transferability to other family members whereas 529 plans allow transfers to most family members, even grandchildren that aren’t born yet.

- Prepaid plans typically require funds to be used by a certain age, e.g., 26 whereas 529 funds can be used when the beneficiary goes back to truck driving night school at age 50 (if said truck driving school is accredited).

- Prepaid plans may place limitations on use and transferability if you move out of state (permanently, not so much for a PCS.)

- Prepaid plans cannot be used for purchases such as computers and software.

- Prepaid cannot be used for off-campus housing.

Which is best for you?

Prepaid plans are not inherently bad compared to 529 plans. Conceptually, prepaid plans:

- Limit loss—they’re not subject to market volatility.

- Drive saving behavior by nudging you to pay the bill like any other household obligation.

- Secure a minimum viable funding level by assuring you of state school tuition.

For these benefits, you give up

The chance to out-earn inflation and “run up the scoreboard” on college savings.

- The chance to spend college savings in more flexible ways.

- The chance to delay spending college savings.

- The chance transfer college savings generationally.

Can I Change my 529 or Prepaid Plan?

If you decide that you want to switch from prepaid to a 529, you may have an option if your state plan allows it. Since you can get a refund for prepaid tuition, it’s easy to switch to a 529. It may also be practical to change how much prepaid tuition you’re aiming at so you can divert dollars to a 529 for additional saving.

Cleared to Rejoin

Prepaid plans have their place and if you already have one, it’s important to get your math on to determine if a switch makes sense. They trade flexibility for a level of security and they “force” savings. For most families, a 529 offers a greater chance of outpacing inflation along with spending flexibility. Regardless of where you are in your college savings journey, it’s never a bad time run the numbers, check your assumptions, and see what may have changed with the flight plan you’re on!

Fight’s On!

Winged Wealth Management and Financial Planning LLC (WWMFP) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Winged Wealth Management and Financial Planning (referred to as “WWMFP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute WWMFP’s judgement as of the date of this communication and are subject to change without notice. WWMFP does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall WWMFP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if WWMFP or a WWMFP authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.