How to Shape a Taxable Portfolio  How to Fix a Taxable Portfolio

How to Fix a Taxable Portfolio

Whatever the reason: your heart or the season, it’s quite common to end up with a taxable account that has all of the rhyme and reason of a football bat.

Perhaps your taxable account has dozens of securities in it and you no longer have the bandwidth to follow them all. Perhaps you bought the new hotness that your shoe shine boy told you about and it no longer fits your investment plan. Or perhaps, as you learned more about how to integrate tax planning and investing, you realized that you’re leaving the IRS a tip with the way you’ve structured your investments.

The first step on the path to fixing a taxable portfolio that doesn’t look like what you’d buy today if you were starting over with cash is to admit there’s a problem. It may not be easy to shape the portfolio, and it may take years to truly optimize it—but the best time to plant a tree was 20 years ago and the second-best time is today.

What’s Wrong with my Taxable Portfolio?

If your taxable portfolio is small, let’s say only a few thousand dollars—and you view it as Vegas money or a “playing-around account,” then the juice may not be worth the squeeze to re-shape it. But if your taxable account has 4 or more zeros before the decimal point, you might want to read on…

Common problems in taxable accounts include:

Underperforming, Actively-managed, Class-A Share Mutual Funds: It’s common to find these pigs loafing around in portfolio that a commissioned (insurance?) salesman masquerading as a financial planner managed/sold at some point. Not that there can’t be over-performing funds in this category such that the sales charges and expense ratios are worth it, but you’ll have to spend a lot of time in math-denial to look past the historic underperformance of most of these funds.

Single Stocks: If the single company stocks in your taxable account don’t fit your investment plan, it would be nice to replace them with a few clicks like you can in an IRA/401(k). But in your taxable account, there’s a solid chance that since 2009, your single stocks have some serious capital gains that will be taxed upon sale.

Bonds and REITS: The income from most Bonds/Bond Funds and REITs is taxed at your ordinary income rate (likely 22%/24% until 2026). The gain from the sale of stocks, ETFs, and mutual funds is taxed at capital gains rates—usually 15%, but potentially 0%.

Recognition of Income: Mutual funds, even index mutual funds, usually pay out dividends and distribute capital gains each year. Regardless of which rate these are taxed at, if the tax was avoidable, then it causes tax drag on the portfolio overall. It’s potentially an optional tax, so why pay it any longer than you have to? (Remember, stocks can distribute dividends too.)

Undesirable Asset Allocation: Asset allocation is one of the 5 Pillars of investing. It’s not uncommon to load up a taxable account with say, all large-cap funds and stocks (Large cap companies are those valued at over $10B). While it may be possible to adjust one’s total portfolio to offset against this, it may not be completely achievable based on account size differences if an IRA or 401(k)/TSP balance is smaller than the taxable balance.

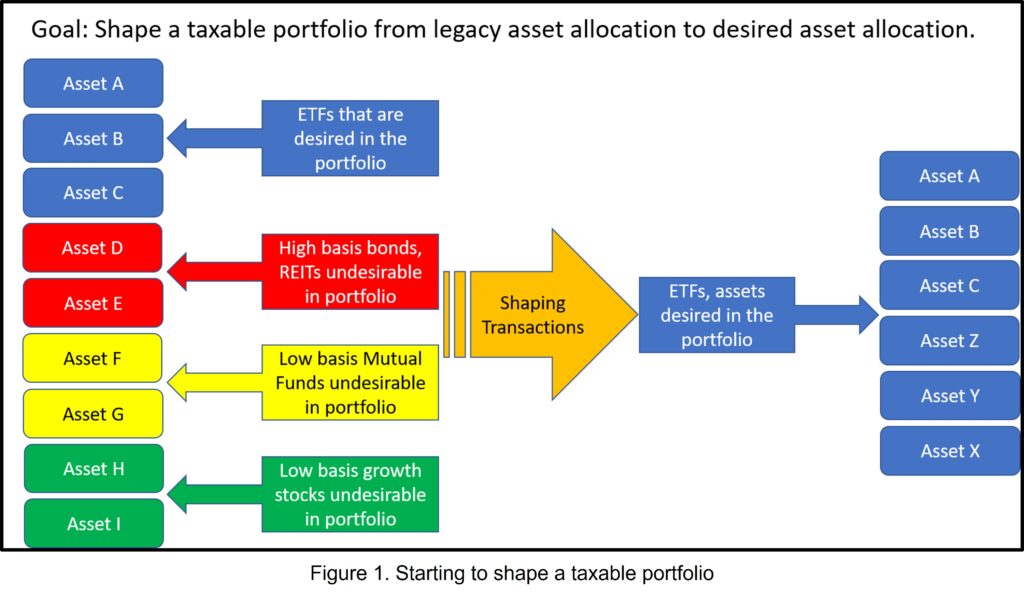

Tools to Shape a Taxable Portfolio

The problem we’d like to avoid when shaping a taxable portfolio is a large tax bill from just selling everything to cash and then buying the new holdings that we want. That’s almost certainly leaving the tax man a tip. While it’s sound wisdom to not let the tax tail wag the investment dog, there are boundaries to that axiom.

Sell at a Loss: Tax Loss Harvesting (TLH) is the act of selling shares that are currently trading at a loss to the price you purchased them. This may not purge 100% of the shares of the unfavorable asset, but it helps. TLH has the added advantage that it creates an offset to any realized capital gains and up to $3K of ordinary income.

Sell at a Small Gain: When you look at the various share lots you’ve purchase (directly or through reinvested dividends and capital gains), you may find that some shares have miniscule gains. Selling those particular shares will generate miniscule taxes and could help prune the edges.

Use the 0% Capital Gains Rate: Long-term Capital Gains are taxed at 0%, 15%, or 20% based on your taxable income. In 2023, if your taxable income is below $89,250 (married filing joint), then gains are taxed at 0% until those gains put you back over $89,250. So, if you have a low-income year, it can be a great time to tax gain harvest at 0%.

Donate to Charity: If you’re charitably-inclined, donating appreciated shares of assets either directly, or through a Donor Advised Fund (DAF) gets capital gains out of your portfolio and harvests a potential tax deduction. If you were going to donate cash anyway, then use the cash to purchase the assets that help re-shape the portfolio.

Patience: This may be the most crucial tool. The portfolio probably didn’t become a misshapen abomination overnight. It’s not getting fixed that fast either. It could take years to fully reshape a portfolio if you’re trying to look skinny to the tax man. It’s possible you’ll never get it 100% to the desired state and that’s okay too. There’s no perfect portfolio anyway.

Die: Making the worm-food transition is last for a reason. While not a serious tool for shaping a portfolio that you’ll own for decades, it’s important to know that assets receive a “step-up in basis” at death. If you bought company ABC for $10 and it’s worth a bajillion when you die, your heirs receive it as though they just purchased it for a bajillion dollars. They can sell it immediately for no taxable gain. It’s very possible that some elements of your taxable portfolio can just hang around until you pass away without causing too much tax drag.

Methodology

There’s no one-size-fits-all solution to this process, but let’s take a look at a reasonable approach. Let’s assume that the portfolio in question has a sizeable amount of capital gains built in, such that just selling to cash and starting over would be a higher tax bill than the expected amount of tax drag over the years.

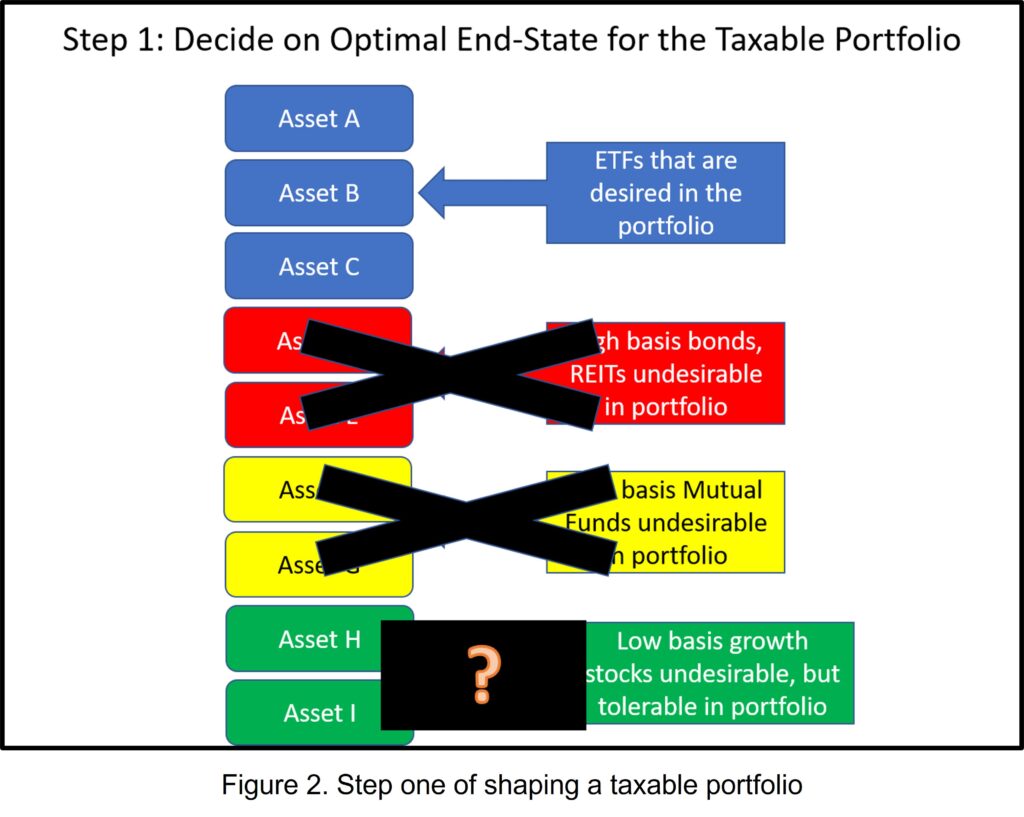

Step 1: Decide what your optimal taxable portfolio should look like. I.e., if you aim at nothing, you’ll hit it every time… begin with the end in mind… etc. Maybe don’t consult the same shoeshine boy that got you here…

If you do consult a professional, consider the conflicts of interest in the relationship. Seeking a fiduciary that is compensated for hourly advice and accepts no commissions or referral fees is a good place to start.

Remember that we generally don’t want REITs and taxable bonds/bond funds in our taxable account. Exchange-Traded Funds and non-dividend paying stocks are usually good candidates for inclusion in a taxable portfolio.

Consider too, that holdings with sizeable gains may be hanging around for a long time, if not permanently, so your ideal portfolio may contain legacy holdings for the long run too.

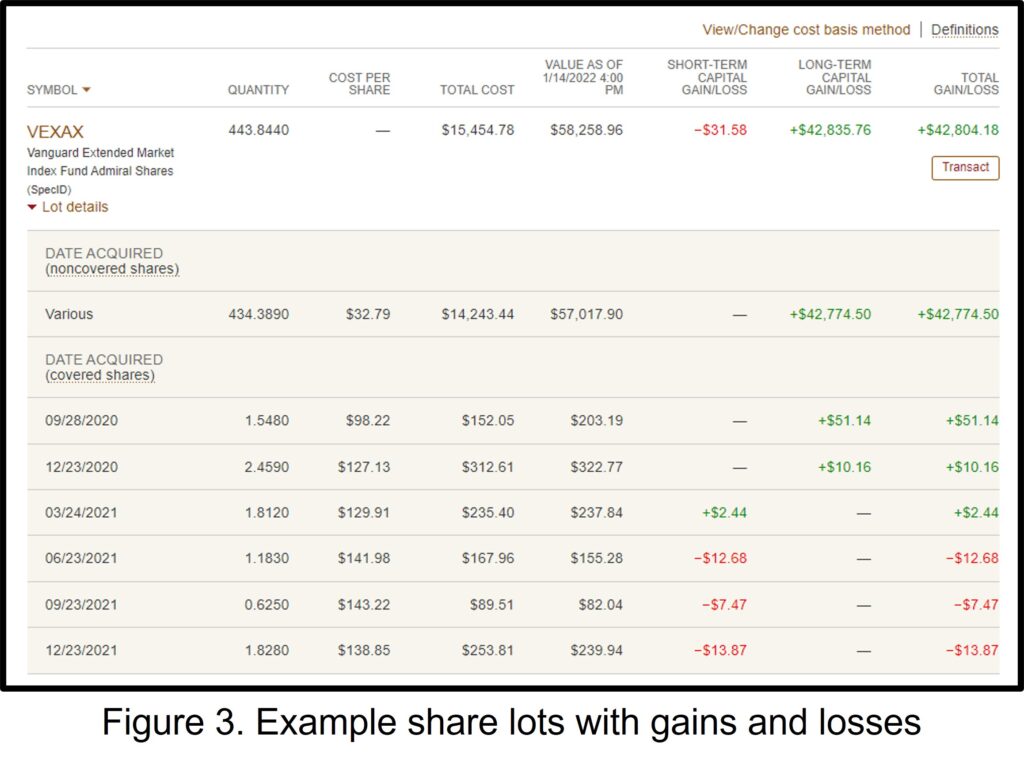

Step 2: Review the unrealized gains for all assets. The process for this will be different at each brokerage. Figure 3. above illustrates an example Vanguard holding. Things to note:

- The bulk of the holding is from pre-2012 when companies did not have to offer tracking by share lot purchase.

- The long-term gains are pretty minimal for the shares from 2020.

- The shares with losses would produce short-term losses. These would first net against any short-term gains before potentially netting against long-term gains.

- Selling the whole asset would produce a tax bill of $6,421 in the 15% long-term capital gains bracket.

Now that you’ve reviewed all of your holdings to understand where your unrealized gains and losses are, you’re ready to start throwing switches.

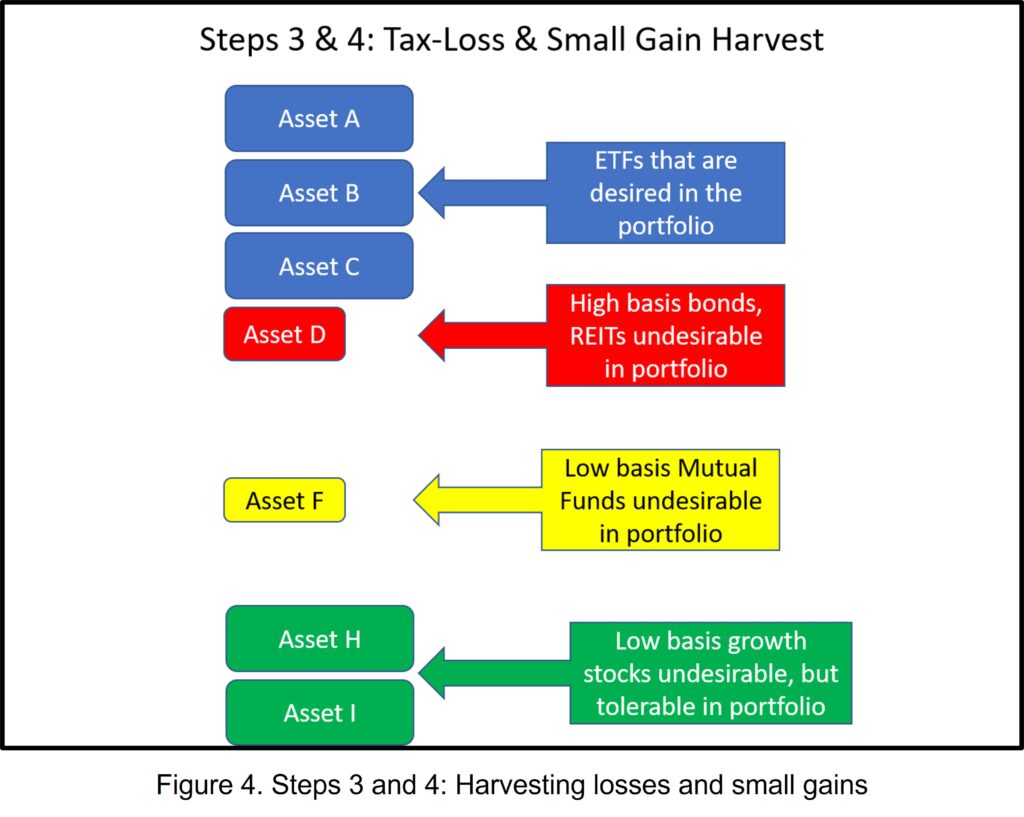

Step 3: Harvest the low-hanging fruit by selling all shares with losses. This tax-loss harvesting is win-win when you’re intentionally shaping a portfolio. Use the proceeds to begin purchasing your desired assets.

Step 4: Sell high-basis shares. While this will produce a taxable gain, if the gain is minimal, it may be worthwhile to get the process moving along. You don’t want to make the process of shaping your taxable portfolio into a new day job. Use the proceeds to begin purchasing your desired assets.

How to Fix a Taxable Portfolio

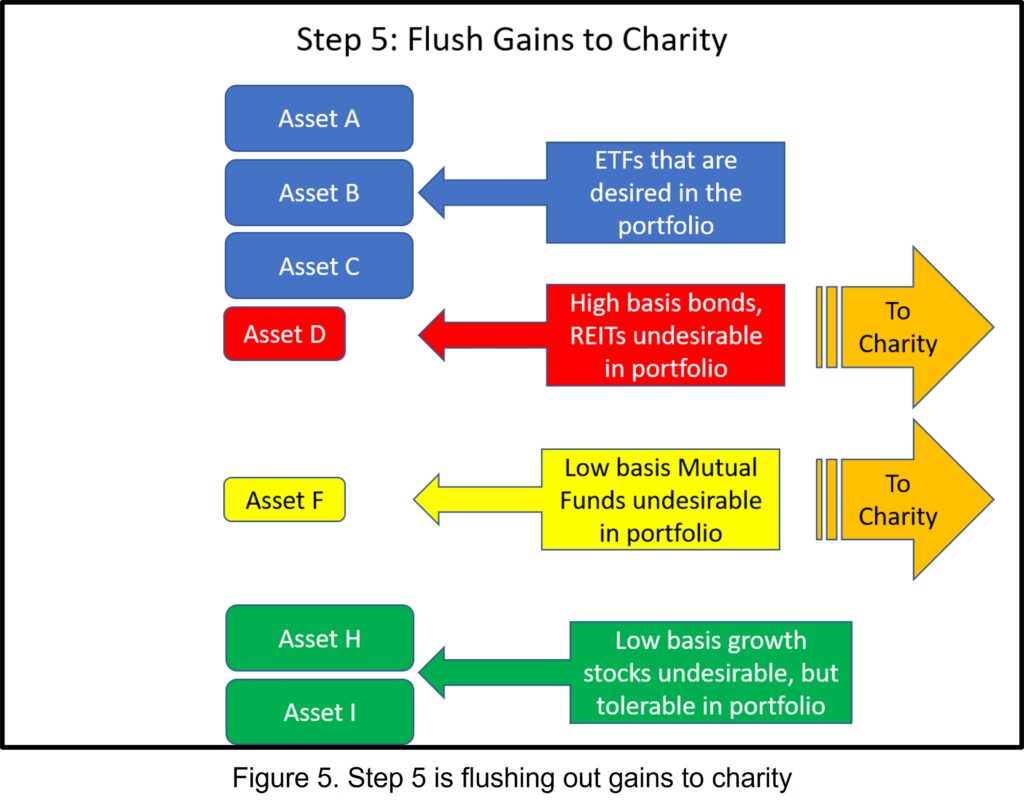

Step 5: (Optional) Donate low-basis shares to charity or your DAF. If you choose to donate shares, picking those with the lowest basis does the heaviest lifting by removing the most unrealized gains from your account. Use cash that you would have donated to charity to begin purchasing your desired assets.

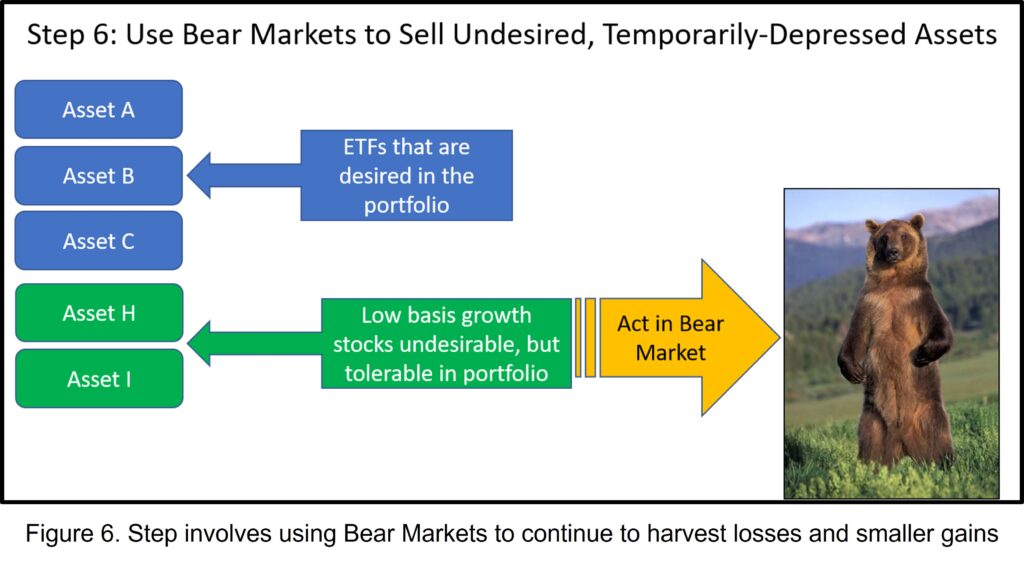

Step 6: Watch for Bears. Market declines are the perfect time to reshape your taxable portfolio. While the rest of the world is chicken-littleing about the apocalypse, use those nerves of steel of yours to execute the plan! You’re basically back at Step 3, but you suddenly have groups of shares trading at a loss.

Step 7: Be patient. Even with 2022’s dismal market, we’ve had a historic run-up on asset prices from 2009 until now. My crystal ball isn’t so broken as to think we won’t have market declines again. Historically, one of every three years has a market correction of 20% or more. You have a plan and a Bear sighting is your trigger for action.

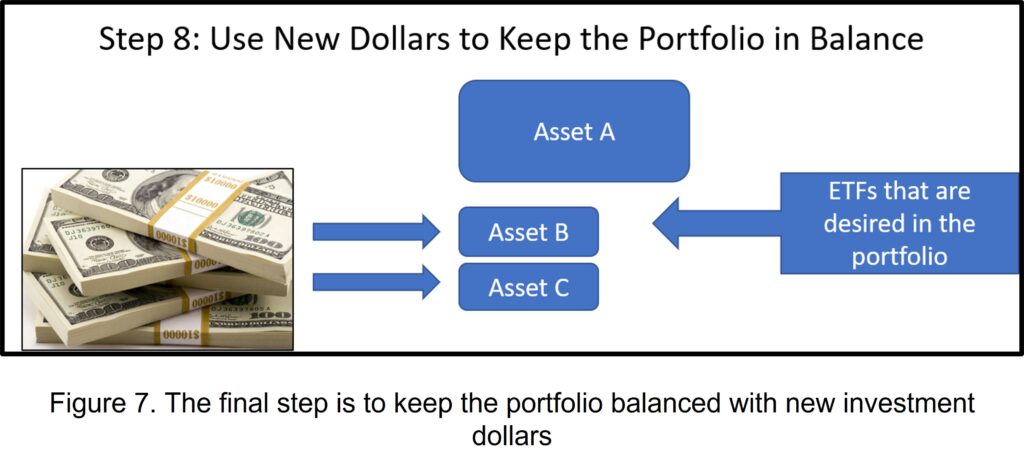

Step 8: Deploy new cash in line with your desired plan. Remember that we don’t rebalance in a taxable account the same way we do in a TSP/IRA/401(k). Ongoing shaping looks like purchasing more of the lower-priced assets and tax-loss harvesting those with gains. This ongoing going shaping takes place at 2 times: when cash is available to invest and when an out-of-balance asset’s price declines.

Finally—lather, rinse, repeat. You can imagine that years of share purchases at various prices, plus years of reinvested dividends and capital gains could create sizeable workload to shape the portfolio.

Cleared to Rejoin

Paying taxes owed is a legal obligation. Paying extra taxes because of an inefficient portfolio is an unforced error. Shaping a taxable portfolio isn’t difficult, but it’s probably going to take time and several iterations of the grind to get the leading edge where you want it. Why not start today by mapping out what you’d want your ideal taxable portfolio to look like and then evaluating your built-in gains?

Fight’s On!

Winged Wealth Management and Financial Planning LLC (WWMFP) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Winged Wealth Management and Financial Planning (referred to as “WWMFP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute WWMFP’s judgement as of the date of this communication and are subject to change without notice. WWMFP does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall WWMFP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if WWMFP or a WWMFP authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.